A post on Facebook got us boatloads of questions related to banking – How do banks make money, What are the different types of banks, what is the primary source of income for banks, how do banks make money, and what is their business model! (and this was only the start!).

We expected very little response but got a superb one – like expectation vs. reality where the reality is better – Just like for Mr. Bean.

Now that we have a ton of questions to answer let me break them down to their nuts and bolts and get into the depths of the banking business model and what their sources of revenue are.

“It is well enough that people of the nation do not understand the banking and monetary systems. For if they did, there would be a revolution before tomorrow morning.”

Henry Ford – CEO, Ford Motors

What are the Different Types of Banks?

All banks work in a fundamentally similar manner. Their business is MONEY. But how they use money as their product differs, giving them different names in the industry. Here are the different types of banks that are common to the general public.

- Central Banks

- Public Sector Banks (PSU)

- Private Sector Banks (PSB)

- Co-Operative Banks

- Regional and Development Banks

- Payments Banks and Digital Banks

- Exchange Banks

- Investment Banks

There are always going to be newer types of banks around the world as the time passes, so we’ll continue to update this page.

How do Banks Make Money?

Banks make money on money. This part is easier said. The tricky part is understanding “how” they do it.

And the exciting part: How can you make money on your money?

Banks offer attractive interest rates, so customers save more money in the bank. Similarly, banks provide offers on loans and credit cards to increase borrowing. This is their product and service cycle, which we’ll understand. Banks sit in the middle and earn an almost risk-free revenue in the billions, if not more!

What is the Main Source of Revenue for Banks?

Banks earn maximum revenue from the loan (debt) and customer deposits that happen as a part of their business model. Money deposited by customers in their savings accounts is used by the bank for investing in debt.

A part of the interest that’s earned from the loans is given out to customers for saving their money with the bank. All interest collect over and above the base rate is revenue for the bank.

Here’s an example:

- Banks in India offer an average interest rate of 4% on saving accounts.

- The average interest for a personal loan is about 11%.

- So the expected income for a bank is 7% of all the money that’s paid out as personal loans.

- Banks earn the most with credit card debts (more on that next…)

How Do Banks Make Money on Credit Cards?

A credit card is one of the most used debt instruments in the consumer market. Even after the decline in their usage, according to Gallup, the average American has 2.6 credit cards.

But the data includes 29% of the population without debit cards.

Excluding the data, the average number of credit cards per person goes up to 3.7!

Banks make money on credit cards by being the middle-person and taking a big cut of 8-15% on the credit card interest rates. Knowing that only 48% of the people pay in full while the rest pay in-part, banks earn most of their revenues from credit card users.

How do Banks Earn Profit on Salary Accounts?

Salary accounts have features like no minimum balance, higher interest rates, cashback on shopping with select brands, domestic air travel discounts, and so much more.

And they’re okay with you have no money in the account whatsoever.

How do banks make money with zero balance salary accounts then? When you open a salary account, your employer allows you to open an account in a specific bank. That’s because the company is affiliated with the bank, and has its bank account there.

Depending on the arrangement with the company, the bank requires one of the two things:

- The entire amount (total salaries of all employees)to be credited to the company’s bank account 7-12 days before the day of the payout

- A percentage of the transaction as a commission

If the money is credited 7-12 days prior, the bank just generated a few million dollars in a float that they can earn interest before paying out.

Else, the commission deducted will automatically be huge enough with the amount of money transacted.

Difference Between Current Accounts vs. Savings Accounts

The two common types of accounts available for bank customers are savings accounts and current accounts. Let’s understand the main differences between them.

| Savings Account | Current Account |

| Suitable for salaried employees or people with a fewer number of transactions per month. | Great for business people or traders who have high-frequency transactions. |

| Interest rates ranging from 3.5% to 6% on the money in the bank | No interest in the money in the bank. Some banks offer minimal interest. |

| Can have lower minimum balance requirements | Usually very high minimum balance requirements. |

| No overdraw facilities. | Accounts can be overdrawn. |

How Does a Bank Make Money on Savings Accounts?

Savings accounts are created for people to keep their money in the bank. This is made possible by offering higher interest rates, guarantees of capital protection, and allowing instant withdrawals with the use of debit cards.

Apart from that, account owners are also encouraged to invest in fixed deposits and recurring deposits by offering higher interest rates.

How do Banks make money on savings accounts, fixed deposits, and recurring deposits? Banks make money on these accounts by lending it out to borrowers.

Here the lending differs based on the type of account – Fixed and recurring deposit money can also be lent out to higher-risk borrowers since the banks have more time to recover the money in case of a default.

Money in the savings account needs to be lent out as short term loans or low-risk loans.

This allows them to earn about 18-25% interest for high-risk lending while the saving account owners get their capital protection with a few percent higher capital gains on their fixed deposits.

Banks have a very cool business model indeed!

What Do Banks Invest in To Make Money?

Now answering the big questions

- How do banks make money and what do they invest in?

- Can you invest in these assets to earn higher interest rates?

Banks invest in debt, and money market instruments to keep the money safe and maintain liquidity while also earning higher interest rates of about 9-10% (or even more).

If you know how to invest in Mutual funds, you can also invest your money in these debt and money market mutual instruments and earn similar interest rates with minimal risks.

Here are a couple of debt and money market mutual funs that I personally invest in:

- IDFC Government Securities Fund

- HDFC Short Term Debt Fund

- Corporate Bonds – As and when they’re available for investments

You can only stick to the mutual funds if you do not want to manage the individual bonds manually.

How do Banks Make Money on Debit Cards?

Debit cards generate a fairly decent amount of revenue for banks. Banks make money on debit cards in the following ways:

- Debit card annual fees

- Transaction charges on ATM withdrawals

- Monthly or Quarterly fees for SMS alerts

The SMS alerts can be charged as bank account fees or debit card fees depending on the bank that you hold and account with. In my case, the charges are added as debit card fees.

How do Banks Make Money on Negative Interest Rates?

- A negative interest rate is when the lender pays the borrower money for borrowing money. A very unusual scenario and extremely unlikely to occur. However, a negative interest rate is a concept that occurs in case of an economic deflation (more here).

But in the likely case that this happens, you might as well be able to finance a car while earning a little bit of money on it! Pretty cool, ain’t it!

But how do banks make money on negative interest rates?

Compared to everything we discussed before, the exact opposite is true in this case.

- Banks charge you to keep money in savings account instead of paying you interest.

- On the other side, you get paid interest for borrowing money.

This condition takes place to ensure higher borrowing and spending so the economy gets a boost again.

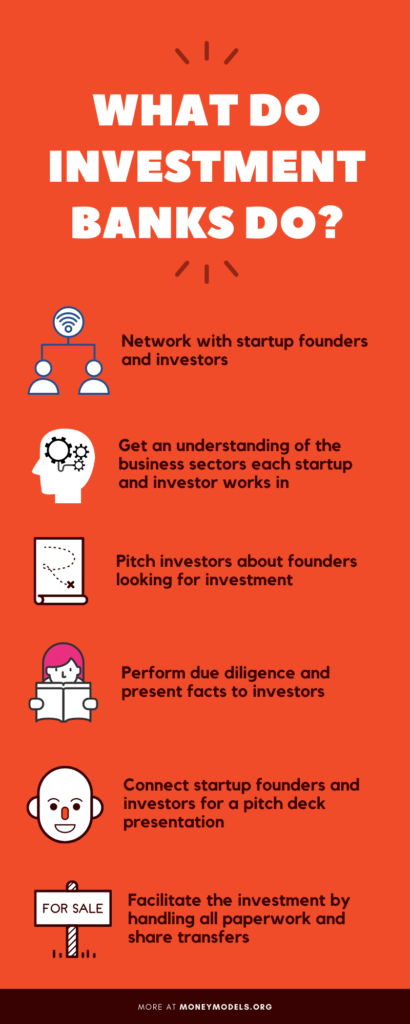

What Does an Investment Bank Do?

Investment banks are a completely different game. They’re not meant for consumers but for investors and businesses. These banks act as intermediaries for businesses looking for investment, and investors looking for viable businesses to invest in.

So how do these banks make money? Well they aren’t doing the hard work for free, are they?

Investment Banks undertake the following tasks:

- Network with startup founders and investors

- Get an understanding of the business sectors each startup and investor works in

- Pitch investors about founders looking for investment

- Perform due diligence and present facts to investors

- Connect startup founders and investors for a pitch deck presentation

- Facilitate the investment by handling all paperwork and share transfers

How do Investment Banks Make Money?

When the investment is facilitated by the investment banks, the banks take a cut from the total investment. This is similar to the brokerage charges that are deducted by the real-estate brokers after the completion of a deal.

These charges come up to hundreds of millions if not more when all the deals are combined. The commissions aren’t fixed and are completely based on what the amount of the transaction is and the contractual agreements between the three parties.

The commissions can also be charged on top of the service charges charged by investment banks which can go up to a couple hundred thousand dollars per deal based on the amount.

Now, every investment banker in an investment bank needs to search for such deals and make pitches to both the founders and investors.

But apart from their salaries, why would investment bankers be motivated to do more than what’s the minimum expected of them? Let’s find that out!

How do Investment Bankers Make Money?

Investment banks charge a commission from both the founders and the investors on the full amount of investment. The service charges of the investment banks add up to a couple hundred thousand dollars per deal.

But how do investment bankers make money and why are investment bankers so rich?

For each deal that’s searched and executed by an investment banker, the banker earn a hefty commission for themselves. This commission can range from 1% to 5% of the investment value.

For a banker who facilitates a $10 million dollar deal, a 1% commission means a $100,000 in pocket for the investment banker.

But these are very conservative estimates and that’s a very good reason why investment bankers are seen driving around in really expensive cars! Damn I really want to become an investment banker now (if it really was that easy xD)

This brings us to the last part of understanding how banks make money. The question is, how do banks make a profit?

If you’ve read through the entire article, you must have a perfect picture in mind of how banks are making money for their operations and for themselves.

Here’s a quick summary of the bank business model.

- Banks pay interest on savings accounts to encourage saving money

- The saved money is used for lending where higher interest is charged to the borrowers

- The difference between the lending interest (8% to 30%) and the savings interest (3% to 6%) is pocketed by the bank for their operations

- Collectively, the amount goes into hundreds of millions even for smaller banks. For national and international banks, the collected interest can easily scale up in the billions

Conclusion

I’m sure you now have a solid understanding of how banks make money and what the bank business model is. This was one of these nagging questions I had for myself quite a few years ago and finally found an answer for myself. But since I couldn’t find a complete answer about how different types of banks make money, I decided to make it happen!

I really hope you had just as much fun reading this article, as I had while writing it! If you have any questions, do not hesitate to get in touch with me through the comments below.If you’re interested in reading more about different business models, don’t forget to check out how Sodexo makes money, the MEGA business model, and how Nearbuy makes money.

Read Further:

![Read more about the article How Does BharatPe Make Money? [Business Model Case Study]](https://moneymodels.org/wp-content/uploads/2023/03/How-does-BharatPe-make-money-300x150.png)

![Read more about the article IaaS Business Model [Easy Explanation]](https://moneymodels.org/wp-content/uploads/2020/12/IaaS-Business-Model-300x125.png)

![Read more about the article How does BeReal make money? [Updated]](https://moneymodels.org/wp-content/uploads/2023/01/How-does-BeReal-make-money-300x150.png)